Your 2022 Social Security Guide

If you’ve dipped your toe into retirement planning, you know it can be an overwhelming process. Even though you’re excited to start a new chapter of your life, you may be stressed about how to make it happen and confused about navigating Social Security. It can be especially difficult when it seems like everyone else has it figured out except you. We get it.

But with record numbers of retirees expected as the baby boomer generation collectively reaches age 65, (1) it is more important than ever that you fully understand how your benefits work—and how they can be maximized. With this comprehensive guide, we hope to help our clients feel confident and prepared to make the most of their Social Security benefits as they enter the next stage of their lives.

How Are Social Security Benefits Calculated?

Your Social Security benefits are calculated based on lifetime earnings. The Social Security Administration (SSA) calculates your benefit based on your 35 highest earning years, with a minimum of 10 years of work required to be eligible for benefits. If you have worked less than 35 years, your earnings will be calculated with zeros for the years you have not worked. All past wages are indexed to today’s wages in order to accurately reflect wage growth.

Once your average monthly earnings for your top 35 years are calculated, a special formula is applied and the result is your primary insurance amount (PIA). The PIA is the benefit you are eligible to receive when you reach full retirement age (FRA).

The actual benefit you receive may not be your PIA. Your PIA will be increased or decreased depending on when you choose to receive benefits. Taking benefits before FRA will reduce your benefit, and waiting until after FRA will increase your monthly benefit. Also, starting at age 62, your eligible benefits will receive regular cost-of-living adjustments (COLA).

Spousal Benefits

Married people are eligible for benefits based on their spouse’s work history. The spousal benefit is 50% of the working spouse’s earned benefit. In order to receive these benefits, the working spouse must be at least 62 and have already filed for benefits.

If you are divorced, you may also be eligible to receive spousal benefits based on your ex-spouse’s work history. Your marriage needs to have lasted at least 10 years, you must be divorced for at least two years, and you must still be single. In addition, you need to be at least 62 and not eligible for higher benefits based on your own work record. Unlike spousal benefits for married people, your ex-spouse does not need to have filed for benefits in order for you to claim them.

When Can You Claim Social Security Benefits?

You can claim your Social Security benefits anytime between age 62 and age 70. If you continue to delay taking benefits after you reach age 70, there is no additional benefit increase. However, the age at which you choose to collect benefits before 70 will impact the amount of benefit you receive.

Early Retirement

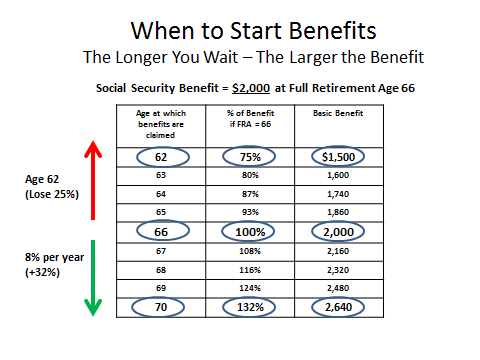

You can start receiving benefits as early as 62, but your monthly benefit will be lower than if you waited longer. Your basic benefit is reduced a fraction of a percent for each month you begin receiving benefits prior to full retirement age. Retiring early can permanently reduce your benefit by up to 30%.

Full Retirement Age

Your full retirement age (FRA) changes based on the year you were born. FRA is 66 for those born between 1943 and 1954 and increases by two months for every year after that you were born until it settles at age 67 for those born in 1960 or later. If you wait until you reach full retirement age to begin collecting your Social Security benefits, you will receive the full PIA that you have earned.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Delayed Benefits

If you’re still working or don’t need the money immediately, you can delay receiving your benefits. Your benefit will increase by 8% for each year that you delay, with a maximum possible increase of 32%. You cannot delay and increase your benefit indefinitely, though. Once you reach age 70, the amount of benefits you receive will not increase any further.

When Is the Best Time to Claim Social Security Benefits?

While you are working, you can increase your future Social Security benefits by earning higher wages. Once you stop working, though, the only influence you have over your benefit is when you begin to take it. Your timing has a great impact on the amount of the benefit you will receive and should be carefully considered.

Social Security Statement

An important document that you will reference during the decision-making process is your Social Security statement. The Social Security Administration mails statements to workers age 60 and over who aren’t receiving Social Security benefits and do not yet have a my Social Security account. These statements will be mailed out three months prior to your birthday, but you can also access the same information by setting up an account on their website.

The statement will tell you your:

- Estimated benefit if taken at age 62

- Estimated benefit if taken at FRA

- Estimated benefit if taken at age 70

- Estimated disability benefit

- Estimated family and survivor benefits

- Medicare information

- Earnings history

All benefit amounts listed are estimates and subject to change. They are calculated based on your date of birth and future estimated taxable earnings.

It’s important for you to review your earnings history and check for accuracy. Your benefit is calculated based on those numbers, so any mistakes can affect your benefits. You should correct any errors as soon as possible.

Deciding When to Claim Benefits

Your Social Security benefits are calculated using complex actuarial equations based on life expectancy and estimated rates of return. They are not designed to encourage early or late retirement. If you live as long as anticipated, the total amount you receive over your lifetime should be about the same whether you claim it at age 62, age 70, or sometime in between. You will either receive the money as a smaller monthly payment over a longer period of time or a larger monthly payment over a shorter period of time.

The best time for you to claim your benefits depends on your personal situation and health. If you expect to live longer than average, your overall lifetime benefit will be greater if you delay claiming your benefits to increase your benefit amount. If the opposite is true and you see little chance of making it into your mid-80s, you would likely receive a greater lifetime benefit by taking it sooner, even though it would be a smaller monthly payment.

Once you decide when you want to start receiving benefits, remember to complete your application three months before the month in which you want your retirement benefits to begin.

How Can Married Couples Maximize Benefits?

Because married people have the ability to receive their own benefit or a spousal benefit, they have more to consider when filing for benefits. With the right strategy, married couples can maximize their benefits.

In the majority of cases, the lower-earning spouse may want to begin collecting benefits early while the higher-earning spouse waits as long as possible. That way, you can access the lesser benefit while maximizing the higher benefit.

Often, it is the husband with the higher benefit and the wife with the lower one. Women also tend to live longer than men. By following this strategy of waiting as long as possible to claim the higher benefit, you not only maximize the husband’s retirement benefit for use while he is alive, but it also maximizes the wife’s survivor benefit when he passes away.

Restricted Application

While it used to be a popular claiming strategy, the Restricted Application is now only available to those born before January 2, 1954. By restricting your application, you can receive a spousal benefit if your spouse is already collecting benefits while allowing your own benefit to continue to grow until age 70. That way, you can begin to receive spousal benefits while maximizing your own benefit.

How Does Working Affect Benefits?

Working does not affect your benefits once you reach FRA, but it does before that. Only earned income, such as wages and self-employment earnings, affects your Social Security benefits. Income from investments, pensions, and annuities do not affect Social Security benefits.

When you are under FRA for the whole year, your Social Security benefit is reduced by $1 for every $2 you earn over $19,560. (2) In the year that you reach FRA, your benefit is reduced by $1 for every $3 you earn over $51,960. (3) Once you reach FRA, your benefit is no longer reduced no matter how much you earn. These dollar amounts adjust each year, so your benefit may change in following years.

Changes for 2022

In 2022 the COLA is 5.9%, the biggest increase in 40 years. Individuals can expect benefits to rise by an average of $92 per month, while married couples will see a $154 benefit increase. (4) There is also an increase to the Social Security tax cap. The cap is increased by $4,200 to $147,000, (5) meaning Social Security taxes will not be withheld from income earned above that amount.

Get Help With Your Social Security Benefits

Depending on how much you have in savings, when and how you claim your Social Security benefits could very well be the most important retirement decision you make. Because of the significance and complexity of this decision, it is a good idea to consult with a financial professional before beginning the process.

We at The Rosamond Financial Group can help you navigate the Social Security process, allowing you to feel confident and prepared for the next chapter of your life. If you are nearing retirement and have questions about what role Social Security will play in your overall plan, we would love to hear from you. Book a free introductory meeting online to get started today!

About Preston

Preston Rosamond is a financial advisor and the founder of The Rosamond Financial Group Wealth Management, LLC with nearly two decades of industry experience. He provides comprehensive wealth management and financial services to individuals, professionals, and families who enjoy simplicity and seek a professional to help them pursue their goals. Preston personally serves his clients with an individual touch, a sincere heart, and his servant’s attitude is evident from the moment you meet him. Learn more about Preston or start the conversation about your finances with him by emailing smrosamond@rosamondfinancialgroup.com or schedule a call on his online calendar.

______________

(2) https://www.ssa.gov/news/press/factsheets/colafacts2022.pdf

(3) https://www.ssa.gov/news/press/factsheets/colafacts2022.pdf

(4) https://money.usnews.com/money/retirement/articles/social-security-changes-coming-next-year

(5) https://www.ssa.gov/news/press/factsheets/colafacts2022.pdf